Happy New Year to everyone. To start the year, I am providing about double the content of a typical Home On The Course newsletter. I hope the information is useful to you.

The latest migration reports are in from major U.S. moving companies, and peoples’ reasons for moving to some states are hard to divine.

I looked at reports from Atlas Van Lines, published just before the end of the year, and UHaul and United Van Lines, which were reported in the last couple of weeks. Respectively, the most net migrations by state were to Arkansas, South Carolina and West Virginia. That is a bit of a head scratcher: Those three states rank low in terms of employment, their economies and the quality of their public-school systems – data that cover the reasons why most people relocate. Of course, “closer to family” is another top reason. (Source: USNews & World Report)

At #36 of 50, South Carolina ranks slightly higher than the other two states in “employment” (availability of jobs). It also ranks 33rd in its “economy, which beats out Arkansas (40) and West Virginia (48). Arkansas (38th) is modestly better than South Carolina (42) in terms of its schools, while West Virginia ranks a paltry #48. (Note: A Newsweek “quality of life” ranking placed West Virginia in 49th place, just behind Mississippi.)

The mountainous West Virginia – what John Denver described as “almost heaven” in his famous Country Roads – is, indeed, a beautiful state, but behind its skin-deep beauty are obviously some fundamental issues. Yet those reading this who think the grass is greener in, say, South Carolina and Arkansas may not have done their due diligence in terms of insurance costs and the rising likelihood of natural disasters. Hurricanes that have made landfall in South Carolina and the consequent flooding have helped push insurance rate increases up by double digits in each of the last few years. And although Arkansas may not make national headlines for tornadic activity, it suffered 52 tornadoes last year, an average of one every week, its highest number in more than a decade.

United Van Lines reported significant net migration to the cities of Wilmington, NC, and Myrtle Beach, SC, both at 80%. Yet late last year, North Carolina’s insurance companies asked for a 50% increase in property insurance rates in the Wilmington area; and Myrtle Beach residents are already paying 2 ½ times the national average for property insurance, a total of $4,820. And that does not factor in extra flood insurance required for those homes deemed at risk for flooding by insurers and FEMA. (See article below.) Those realities should make some retirees think twice about where to retire.

Some of the other states ranked in the top 10 for in-bound traffic are equally surprising. The Atlas Van Lines report lists Rhode Island (#2), Maine (7) and Connecticut (8) among the top 10. As recently as three years ago, the news media in Connecticut, where my wife and I maintain our primary home and where we raised our children, were shouting about people leaving the state. But with an economy ranked by USNews at #17 and public schools ranked #8, the headlines have quieted. (Note: I know from personal experience in the Hartford, CT, area that the state’s #3 rating nationally for the quality of its healthcare is more than justified.)

The van line reports are more interesting than they are conclusive. They measure only the locations to which they move customers, a vast minority of the numbers of people moving across the nation. But they do raise questions about what kind of research people undertake before they make consequential moves, and what their motivations might be. They can’t all have relatives in West Virginia.

*

As a related footnote that things may not be exactly as they seem in West Virginia, it might surprise some to learn that John Denver’s Country Roads was written mostly by a lyricist from Massachusetts and that the line “Blue Ridge Mountains, Shenandoah River” describes the area immediately to the east and west of Interstate 81; the Shenandoah Valley and Blue Ridge Mountains are in Virginia, not West Virginia. It is entirely possible that the song refers to “west Virginia,” not West Virginia, a credible notion since Denver and his lyricist never set foot in West Virginia.

Remember the old joke that, someday, because of California earthquakes, people living in Las Vegas would eventually own beachfront property – on the Pacific Ocean? The unspoken corollary, of course, was that those currently living beside the ocean would become homeless, or worse.

Although the beachfront-property-in-Vegas riff is still a far-fetched joke, what is happening on the coasts of the U.S., and in other areas vulnerable to much more than earthquakes, is no laughing matter. As they pay out more and more claims for damages caused by natural disasters, insurers are raising rates significantly and, in a troubling number of cases, dropping their coverage altogether.

If you are unlucky enough to own a home in a high-risk location, you likely have felt the pain already. But if you haven’t received a letter from your insurer yet, imagine that you might lose your insurance on a home because of the risk of hurricanes, flooding, wildfires, tornadoes or other potential disasters. Not only could you be forced to self-insure a home that would cost hundreds of thousands to replace, but anyone who might buy it from you would have trouble finding a mortgage company to lend them money if an insurance policy can’t be written for the house.

For some homeowners who hold mortgages, the story is just as bad. Take, for example, Mike Patterson, a teacher in California whose insurance saga was covered by the San Francisco Chronicle. His longtime federally backed insurance policy was cancelled through no fault of his own.

“…[Patterson’s] longtime insurer, California Casualty of San Mateo, was downgraded by a credit rating agency,” the newspaper reported. “As a result, his federally backed mortgage lender would no longer accept his insurance.”

Patterson had no choice but to sign up for coverage from California’s insurer of last resort, the state-backed FAIR Plan.

“Now he pays just over $1,400 for insurance through the FAIR Plan,” according to the Chronicle. “That’s double what he used to pay to get just a fraction of the coverage, and unlike his old insurance, it covers only issues caused by fire.”

Folks who live in the bucolic areas of western North Carolina could not have imagined that natural disasters would cause them to lose their homes, or that they were not covered in total by their insurance policies. And from a hurricane…400 miles from the point of landfall on the Florida coast? Yet the after-effects of Hurricane Helene, which made landfall in August last year where the panhandle of Florida bends to the west, caused billions of dollars in damage and ruined the fortunes of many of western North Carolina’s residents.

Many of the people affected by flooding from hurricane Helene had no idea that their homeowner’s insurance did not cover water damage. In the world of insurance coverage, property damage from wind, for example, is covered in most policies but not damage from flooding. My wife and I pay for a separate flood policy on our condo in South Carolina. It is backed by FEMA and covers flooding that destroys the items people depend on for their survival, such as refrigerators, utilities and other essentials. We carry a separate policy from State Farm that covers furniture and other personal property. The State Farm policy premium in 2024 was $894. The FEMA-backed policy was $1,111. (Note: In 2024, our personal policy premium decreased by a few dollars; the flood policy increased by more than 10%.) Those two policies do not even cover any structural damage or destruction of our two-story condo, which is one in a building of six units. Through our condo association we paid yet another $5,540 last year to cover the potential total loss of the condo. This year we will pay $6,130, an increase of 10%.

Our condo is almost a mile from the Atlantic Ocean as the gull flies and, despite some past hurricanes that damaged our golf course, the condo has suffered no flooding in 24 years. But Pawleys Island, SC, is not Asheville, NC; we expect hurricanes and are under no illusion that some might be especially damaging. The folks near Asheville had to be cruelly shocked by the ravages of a hurricane from so far away.

Insurance companies do not factor that you paid all your premiums on time for decades or that you never filed a claim. Given the increasing numbers of natural disaster claims that they must cover, they can make the case to state review boards that they need to raise their rates. If they deem the risk to your home has increased sharply, they can even drop your coverage; there is not much you can do about it. Insurers have fled states like California and Florida, which have responded with some assistance for the suddenly uninsured. Florida, like California, set up what is essentially a state-run insurance provider to cover at-risk residents whose insurance companies had left the state. The premiums are typically higher than what the homeowners were used to paying, but at least they have coverage. Yet the payouts for any future catastrophic hurricanes might exhaust funds in the state pool, lead to higher rates for those in the state plan and, potentially, lead to higher taxes for all of the state’s residents. (Note: Florida levies no state income tax but the money to fund such shortfalls will have to come from somewhere.)

As I write this, wildfires are raging outside of Los Angeles, leveling trailer homes and mansions alike. Many of the expensive homes are covered by California’s FAIR Plan whose ramifications, according to the San Francisco Chronicle, “could well be felt across California. Most obviously, the massive losses that insurers face could translate to increased rates for people across the state — particularly in the areas affected by the fires but also beyond…The [FAIR] plan has an estimated $24.5 billion in exposure across 15,300 residential and commercial policies in the ZIP codes impacted by the Southern California wildfires,” according to a Chronicle analysis of FAIR Plan data. Last summer, the FAIR plan held reserves of $385 million to pay for claims, according to the Chronicle.

A year ago, the bureau in North Carolina that represents insurance companies argued for rate increases that ranged from 4% in parts of the mountains to 99% in some beach areas. Increases in big cities like Raleigh, Charlotte and Greensboro that are popular with retirees and young families alike were expected at approximately 40%. Yet that was before most of the western part of the state was devastated by Hurricane Helene. In Buncombe County, which comprises Asheville, the rate-increase requests before Helene were for 20.5%. Residents of western North Carolina will almost assuredly have to prepare for more dramatic increases in the coming years.

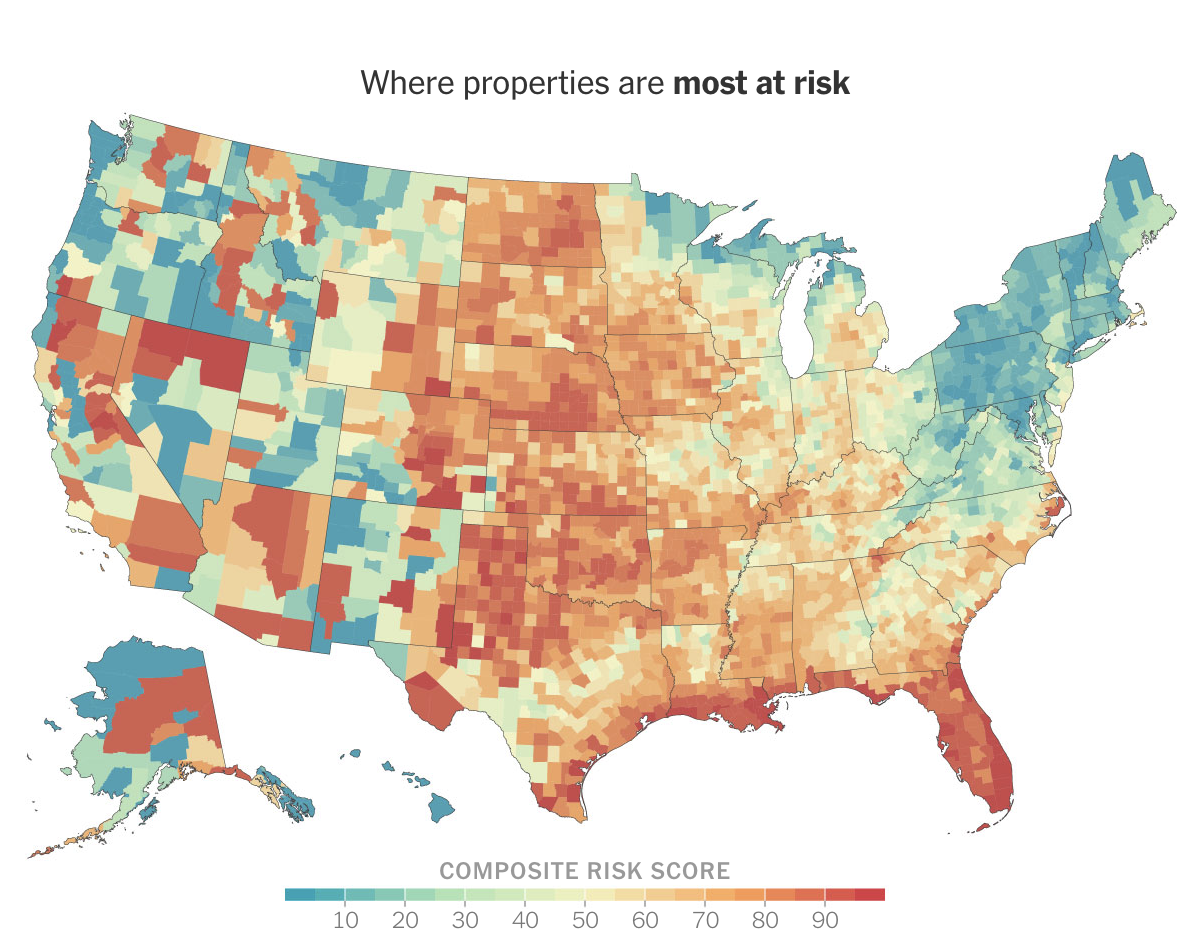

With natural disasters hogging the headlines across the U.S., are there any safe havens left? The map below pinpoints both the hotspots and the relatively safe spots across the land. Note that, in general, the highest risk locations are where retirees relocate for sunshine year round; and the lowest risk areas, like New England, are from where retirees have emigrated to avoid cold winters.

I also asked the following of ChatGPT, the artificial intelligence program: “Create a short article that identifies the places in the U.S. that are safest from the ravages of disasters, including hurricanes, flooding, tornadoes, earthquakes, wildfires and other natural disasters. List at least 10 places that are considered safe and where property insurance rates reflect those conditions.” Note that the 10 “safest” cities are almost exclusively northern; only Charlotte, NC, is in what is typically labeled “The Sunbelt.”

Here are the 10 towns that the program deemed safest, with some short rationales for the choices:

In early August 2023, my wife, my kids, grandkids and I spent a wonderful week on Lake Lure in North Carolina. That picturesque lake, where much of the movie Dirty Dancing was filmed, lies downriver from the town of Chimney Rock, which was decimated by flooding from Hurricane Helene last October. One local official put it this way to NBC News:

“…15 businesses were destroyed and 26 more were damaged. On the south side of town, 15 homes were obliterated and 14 more were damaged. Five bridges, including a footbridge, were razed. Three miles of Main Street, which is also known as U.S. Highway 64/74, were completely torn apart.”

The remnants of buildings torn apart by the flooding were carried down the Rocky Broad River to the circa 1927 dam that protects Lake Lure (photos below). The old dam held, but water carrying the flotsam and jetsam of the destroyed town overflowed the top and sides of the dam and turned beautiful Lake Lure into an unimaginable trash receptacle. Chimney Rock is located in Rutherford County, NC. A FEMA map detailing hazard risks across the country describe the Rutherford County risk as “relatively low.” (You can check out your own county here.)

Lake Lure, summer 2023

Lake Lure, October 2024

Most of the homes around Lake Lure sit at elevations well above the river and the lake. However, some were affected by reported mudslides. While watching my grandson on a putting green next to the community center at Lake Lure, I struck up a conversation with a retired couple who extolled the virtues of living in the community, including the climate. On reflection, it is a sad reminder of the Bob Dylan line: “Don’t go mistaking paradise for that home across the road.”