December is when we look back at the year past and ahead to the coming one. The pandemic has had a profound effect on real estate, especially in high-quality golf communities. Demand is up, supplies are down and even non-economists among us know what that means for prices. That reality could be with us for years to come. We explain. Also, if you are a Democrat, Republican or Independent, there are locations for each of you. But we found a few where everyone, regardless of political persuasion, can be happy. It is all in this month’s Home On The Course.

For nearly 20 years, I have written articles that tout the glories of living in the Southeast, including climate, low cost of living and great golf. I still believe all that and will continue to encourage my readers to consider a home in that part of the country. But some things have changed over the last two decades, not the least of them the pandemic, that convinces me that some of us are looking for alternatives – now, and into the future. And one great alternative is the state of Vermont. Read why in this month’s issue.

The 2021 hurricane season will just be a painful memory a month or so from now. But as we wave goodbye, we should not forget that flooding is becoming more of an issue in low lying areas of the east coast. Witness the mayhem in New York and Philadelphia in the wake of Hurricane Ida. As seas rise and storms become more intense, it is wise for those contemplating a home in the coastal South to review flooding potential. We explain how in the latest issue. Plus, for those who believe that no-income tax states are low tax states, think again. We explain.

The tragic recent flooding in central Tennessee and Louisiana are a reminder that water can have a devastating effect on the lives and economics of home ownership. That is one of the reasons that Realtor.com, the website of the National Association of Realtors, now includes two measures of flooding potential with the homes they list for sale. One is the Federal Emergency Management Agency (FEMA) and the other is Flood Factor, a “tool created by the nonprofit First Street Foundation that makes it easy for Americans to find their property’s risk of flooding and understand how flood risks are changing because of a changing environment.” FEMA’s measure of flood risk covers small geographic areas; Flood Factor assesses the risk to individual homes. They are best considered in tandem as neither is conclusive by itself.

It is undeniable that sea levels are rising annually, last year by .13 inches. That may seem like a small amount but a tenth of an inch here and a tenth of an inch there spread across 41 million square miles, the size of the Atlantic Ocean, and pretty soon you are talking about serious water, with potentially devastating consequences for cities and towns adjacent to oceans. Among coastal cities in the U.S., New York’s population today faces the largest risk of all, according to a report by Climate Central, a group that monitors and assesses public climate data and uses FEMA’s 100-year coastal floodplain as guidance. But New York is an anomaly; of the 25 cities most vulnerable to flooding today, 22 of them are located in Florida; Charleston, SC, ranked the 15th most vulnerable city, and Atlantic City, NJ (#23) are the only ones (other than New York) not in the Sunshine State.

I recently looked at homes for sale at Realtor.com that are located in golf communities near bodies of water. (Note: Flood assessments are located under the “Neighborhood” tab for each listing.) It is important to understand that properties within the boundaries of one community can have different flood ratings, sometimes vastly different. When there is agreement between FEMA’s ratings (two-letter designations) and Flood Factor ratings (10 point scale, 10 being the most risk), the flood risk can be considered reliable.

My wife and I own a vacation condo in Pawleys Plantation in Pawleys Island, SC. Our condo, which is located in about the geographic middle of the community, has a Flood Factor rating of 1 in 10 and a 3% chance of any flooding over the next 30 years. (Over the past few years, the community has endured a few strong hurricanes but no flooding in our condo.) The FEMA rating for the condo is equally positive; we have a 1% chance annually for flooding (or looking at it even more positively, the condo could flood on average once every 100 years). But at the end of our street, just under a half mile away but adjacent to the marsh that separates the community from Pawleys Island and the Atlantic Ocean, the Flood Factor is 10 out of 10, considered “Extreme” and FEMA designation of “AE,” or “high risk.”

Sometimes Flood Factor and FEMA disagree substantially. At Cypress Landing, for example, a Chocowinity, NC, community located beside the Pamlico River, most homes rate a 1 for Flood Factor, the lowest rating available. But a large house with commanding views of the river rates an X500 from FEMA which, essentially, predicts no serious flooding for 500 years and recommends, but does not require, flood insurance. But Flood Factor gives that same home a 7 out of 10 risk for flooding over the next 30 years and predicts at least one inch of water will reach the first floor in the next 15 years. The difference between the two assessments is too wide to be meaningful or helpful.

Realtor.com’s choice to include Flood Factor risks imbues the ratings with considerable credibility. It is worthwhile to consider them but to water them down, if necessary, with FEMA’s own rating.

Every time my wife and I visit our daughter and her family in northern Vermont, we consider buying a modest home for us to be nearer to them, especially with a new grandson born in late August. That cannot be our only home because, well, Vermont winters… We could keep our condo in Pawleys Island, SC, and bounce seasonally between South Carolina and Vermont, or we could opt to own one home and rent seasonally either up north in the summer or down south in the winter. Either way, golf will be played 12 months a year.

I was able to play eight golf courses around Lake Champlain in northern Vermont and New York state in September. Although that area is not rife with layouts, there are enough to keep a two-day-a-week golfer busy and entertained. I have reviewed a few so far at my web site, OffTheBeatenCartPath.com, and will be posting others over the coming few weeks. All the courses have housing options nearby, a few right on the property.

I was struck by how inexpensive annual memberships are. (None charge an initiation fee.) All were under $2,000; even given the relatively short season – beginning in late April and running into October – the cost per round for someone who plays three days a week would be considerably less than the average green fee rate. At the most remote course, Jay Peak, just five miles from the Canadian border and an hour from Burlington, the “weekday” annual rate (Sunday through Thursday) is just $680; play just 11 times during the six-month season and you will pay less than the $65 per round weekday greens fee. (The full-week seasonal rate is $1,500.) Jay Peak is the best public access course in the state, according to Golf magazine, and off of my two rounds there, I cannot disagree. It is wonderful, with excellent conditions in a mountain setting that is drop dead gorgeous.

In my book Glorious Back Nine: How to Find YourDream Golf Home, I suggest that some retirees overtax themselves about taxes. They limit their retirement options under the mistaken notion that they can protect all their retirement income from the ravages of state taxation. They can’t.

The financial part of your retirement is not under assault by state taxation. Your enemy is cost of living of which income tax is just one component and largely irrelevant for folks whose income is under a certain level. As the popular financial newsletter Kiplingernotes and I repeat in my book, no-income-tax states are not the cheapest places to live. Indeed, its lower property taxes and kind tax treatment for moderate-income seniors makes South Carolina, which has an income tax, a cheaper place to retire than Florida, which has none. The average property tax in Florida on a $400,000 home is about $4,000. In South Carolina it is less than $2,500. For folks with annual retirement income of, say, less than $50,000, that $1,500 difference is a big deal.

Tennessee, another state that does not charge an income tax, assessed the highest sales taxes of any state in 2019, according to the Tax Foundation. Tennessee charges a 7 percent sales tax statewide; but combine it with local sales taxes and the rate increases to an average of almost 9.5 percent. For retirees with limited incomes, hefty sales taxes are a larger burden than state income taxes since a large fraction of their income is spent on taxable items.

States cannot function and serve their citizens without a revenue stream. If the money doesn’t come from income taxes, then it must come from other levies. Even then, some of these no-income-tax states must cut corners that, directly and indirectly, make life more difficult for retirees. Retirees with health issues should consider carefully a move to a no-tax state. According to a US News & World Reportranking, Tennessee ranks 43rd in terms of quality of healthcare, Texas 37th and Florida 29th. (Note that no-tax New Hampshire’s healthcare ranking is a decent 16th but you’ll need a winter wardrobe to live there.)

Retirees in the North who choose not to move to Florida like to refer to the state as “God’s Waiting Room.” They may be onto something; the state ranks 10th in most deaths due to the coronavirus, Texas 20th and Tennessee 22nd. Maybe there is a connection between death and (no) taxes.

The course layouts I have begun playing are more than 1,000 yards shorter than those on the PGA Tour. And, yet, the approach shots I am hitting to greens are struck with pretty much the same numbered irons the pros use. (They, of course, can hit a 7-iron over 200 yards; me, not so far.) To a golfer who can no longer drive a ball much farther than 200 yards, having 7-iron approaches is more fun than hitting metal woods off most par 4 fairways. I explore the emergence of hybrid, or combo, tees in this issue of Home On The Course and include a few samples of playable layouts with and without combo tees.

The Reserve at Lake Keowee, Sunset, SC

The Reserve at Lake Keowee, Sunset, SC

I recently posted at my web site, Golf Community Reviews, some thoughts about combo, also called “hybrid,” tees that fill in the gaps between tee boxes on many golf courses. The difference between, say, a layout at 6,500 yards and one at 6,000 yards spread over 18 holes may not seem like much (an average 28 yards per hole), but the longer set can pose multiple 400 yard par 4s that make an iron approach impossible for many of us. But, typically, golf courses that offer those combo tees first trim their 400-yard par 4s to make them reachable in two for those of us who can no longer drive a ball more than 200 yards. (I have joined that 200-yard-maximum group in the last couple of years.)

In the article, I referenced a few public layouts I play in Connecticut. But many of you reading this now either belong to private clubs or hope to in the coming years. Therefore, I have looked at a few private golf community courses to see if the trend has caught on there. The answer is a mixed bag of approaches.

The Landings in Savannah, GA, features six layouts designed by Tom Fazio, Arnold Palmer, Willard Byrd and Arthur Hills. Hills designed the Oak Ridge layout in 1988, and the original yardage from the back tees was a modest 6,600 yards by today’s standards. Its course rating of 72.7 and slope of 135 are also on today’s low end of ratings from the way-back tees. Still, the layout features five par 4s over 400 yards in length, including the two opening holes. The next longest layout, at 6,200, still features five par 4s over 380 yards, making those holes reachable only with fairway metal clubs after a 200-yard drive. Not much fun, that.

The Landings smartly developed hybrid layouts by combining tee boxes to create two additional layouts at 6,103 yards (Tournament/Club Combo) and 5,614 yards (Club/Medal Combo). The longer layout of the two features just one 400-yard par 4 (404 yards) but softens that blow with only one par 5 over 500 yards (504). The longest par 4 on the Club/Medal layout is 374 yards but there are a few under 325 yards, including the finishing hole at 317, down from 368 on the Tournament/Club layout.

The Landings has inserted the combo tees on all its golf courses, a smart move for a population whose average age is retired. The trend has caught on with dozens of other private golf community clubs. (See sidebar for a recap of some of them.)

In some cases, combining tee boxes is not necessary because the original designers and their patrons thought about aging and loss of distance. Twenty years ago, when he designed the course at Glenmore Country Club in Keswick, VA, John LaFoy recognized that most members of the golf community’s country club would eventually be unable to drive a ball 250 yards. He also received key input from the club’s golf professional, a former mini-tour player and daughter of the owner who commissioned LaFoy.

“She understood that not all women have the same capabilities,” LaFoy told me, “and it would be ridiculous to have just one [tee box] designated for women. [Therefore] we built five sets of tees there, which were probably not enough.” (Note: A sixth tee box has since been added.)

At Glenmore, LaFoy designed the white tee layout (6,149 yards, course rating 70.5, slope 138) with no par 4 longer than 400 yards and only one longer than 372 yards. That layout’s slope rating implies it is a significant challenge for a bogey golfer who should consider moving up to the yellow tees, a layout that measures 5,730 yards (68.5, 134), with only one par 4 longer than 380 yards and the next longest at just 356. The other tee boxes are black (7,003 yards, course rating 74.1, slope 146), blue (6,601, 72.5, 142), red (5,223, 66.2, 128) and green (4,061, 61.4, 114).

Hot designer Gil Hanse must have had 200-yard drives in mind when he retrofitted Pinehurst #4, whose prior architects are all hall of famers: Donald Ross, Robert Trent Jones, Rees Jones and Tom Fazio. (Pinehurst offers a comprehensive, reasonably priced membership to any resident of a community adjacent to one of its nine golf courses.) The spread between the white tees (6,428 yards) and green tees (5,864) may seem a bit wide, but the latter layout features par 4s as long as 382 yet balances that with two par 4s shorter than 260 (the fairways on the latter two are ringed with sand).

One golf industry official indicated to me that he thought combo tees were a “terrible idea” because they forced most par 4s on an established layout into roughly the same 350-yard or so box. My own experience, as I have reduced my ideal layout to just below a total of 6,000 yards, is that 350-yard holes do not all look the same or demand the same strategies; they offer different challenges that might argue for different club selections. Where I find the combo tees a problem is in bringing hazards and other obstacles into play for the shorter hitter.

Example: The 5th hole at Pawleys Plantation, designed by Jack Nicklaus, is a par 4 with a three-story tall tree along the left edge of the fairway. (In the 1980s, trees perilously close to or in the middle of fairways were a dubious Nicklaus design signature which he mostly abandoned in later years.) From the back tee boxes on #5, you face a straight shot down the fairway; pull your drive and the tree comes into play. Hit it straight and you are in great shape. But move up 20 yards to the white tee box (350 yards from the green), which is set to the left of the fairway, and the tree is directly in front of you, forcing you to either play a significant draw around it or hit a fairway metal short of the bunkers on the right edge of the fairway. Hit the fairway metal from the white tees instead of a driver, and you face a longer than necessary approach over a pond to a narrow green. The shorter tee box on that hole is a major disadvantage.

Older golf courses facing the need to add tee boxes to accommodate shorter drives must negotiate the delicate balance between keeping the integrity of the original design and providing a fun experience.

“When I retrofit an existing course,” architect LaFoy told me, “I can usually figure out a way for most players to avoid [bunkers] if they hit a fairly decent shot. I try to never line up a forward tee (or tees) that ladies and seniors may play where they have to hit directly at a bunker.”

And that, after all, should be the essential challenge of golf: Not to hit a perfect shot to avoid hazards, but rather a decent enough shot. In the end, if you can only hit the ball 200 yards or so off the tee, a few extra 350-yard par 4s will make for a more enjoyable day than playing a handful of 400-yard par 4s (unless you are in love with your 3 wood) — even if a bunker you could not reach from the back tees will gobble up a poorly played shot. In that case, you deserve what you get. Those who anticipate a loss of distance and are looking for a golf community home they expect to live in as they age would do well to study the course scorecard before they plunk down their initiation fees.

Larry Gavrich

Founder & Editor

Home On The Course, LLC

The following golf courses feature tee configurations that will satisfy those of us who can no longer drive a golf ball much beyond 200 yards. For each course, I picked the tee box most appropriate for such distances, as well as the next one farther back for those of us who can still drive for show. (Course and slope ratings in parentheses.)

I have owned a vacation home for more than 20 years. Did I make a good choice? The answer is a qualified yes. Would I do some things over again. Definitely. I made mistakes. I share some of the most common ones this month in Home On The Course. Also, I identify six communities, half of which will appeal to those who want to be close to the action of a city, the other half where pollution and traffic have no home.

Vermont National, Burlington, VT

Vermont National, Burlington, VT

In my book, Glorious Back Nine: How to Find Your Dream Golf Home, I elaborate on some of the most common mistakes couples make when they search for a golf home. The following are 10 common mistakes and how best to avoid them.

One of the biggest mistakes a couple makes is looking for a golf community that seems nice without understanding if the surrounding area is a good match for them. This boils down essentially to remote location vs near a full-service small city. There are wonderful golf communities in both types of areas, but a remote location may not provide the restaurants, entertainment options and, in some cases, medical care you want. On the other hand, those remote communities won't provide you with traffic and pollution (noise and air) either. Cautionary note about remote living: If you consider that your last 40 years of work and family responsibilities justify a quiet retirement life, understand that there are also hassles with driving a half-hour roundtrip to the supermarket and doing all your other shopping online.

My wife does not play golf but she does like the beach. I prefer mountain golf to coastal golf, but not by a large margin. I have played enough golf in the Carolinas to know that there are fantastic layouts east and west. When it came time to choose a vacation home in the Carolinas, I agreed with Mrs. G that a Pawleys Island, SC, golf community six minutes to the Atlantic Ocean and on a Jack Nicklaus golf course was right for both of us (and for our small children, at the time). We have both been more than content with the choice. Happy Spouse, Happy House. Let the non-golfer make the final decision.

In my 74th year, my distance off the tee has shrunk by more than 25% of its peak when I was younger. In other words, a par 4 400-yard hole today plays the equivalent of 500 yards in my younger days. That was a par 5 for me even back then and is more like a par 6 today. The point here is that the golf course you choose to join today, when you are still flexible and can drive a golf ball well over 200 yards, is not the course you will play in your 60s and 70s. Make sure when you play it before you decide to join the club or the community that the more forward tee boxes are appropriate for when you can hit the ball no more than 200 yards, maybe less. And pay attention to the green complexes; I have become a poor sand player and the Pawleys Plantation course I play features lots of sand. I once shot 74 there from the middle tees; from the forward tees I have only broken 80 once in three years.

If you want to be the big cheese in a community, then by all means search for the most expensive home. But your neighbors may have a hard time warming to the “rich people on the hill.” Better to aim at a $1 million house among those valued at $750,000 to $2 million. The homes in the comfortable middle range tend to hold their values better anyway — during good times and bad.

You don’t want to spend your retirement years trying to keep up with the Joneses. As with more expensive homes (above), target the middle of the price range in a community you like. A $500,000 home in a community whose prices range from $350,000 to, say, $750,000 will provide you with a home of about 3,300 square feet, plenty of room for a fourth bedroom, a dining room (if you want) and a nice office/guest room. Let the Joneses worry that you got a much better deal than they did.

Yes, we know the cost of lumber is out of sight. Add to that a labor shortage, and building a new home appears to be cost prohibitive. But is it? In Pawleys Island, SC, where my wife and I own a vacation condo and a building lot, construction costs in the last year have risen from around $150 per square foot before the pandemic to $200 today. Simple math: A 2,500 square foot home that would have cost $375,000 to build in 2019 will cost approximately $500,000 today. By the same token, existing homes in the Pawleys Island area have increased an average $75,000 over that same period, according to the online real estate agency Redfin. The extra expense to build a home today is around $50,000. But home site prices have not risen as much as resales have, largely because of the lumber crisis. As the pandemic abates, look for tree cutters and sawmills to ramp up production and for the prices to come down. When that happens, if you were to already own a home site — there is a small patio lot for sale in Pawleys Plantation, for example, for just $99,000 — you would be well positioned a year or less from now to build the house you want at a price you can afford.

In 2000, after multiple happy summer weeks spent with our then-young kids in the Myrtle Beach area, my wife and I purchased a condo in Pawleys Plantation in Pawleys Island, about 35 minutes’ drive south of Myrtle Beach International Airport. The Jack Nicklaus golf course on site appealed to my son and me, and the beautiful Atlantic beach just six minutes from the condo was a favorite spot for my wife and daughter (and these days our dog, Coco). To encourage us to purchase the condo, the developer kicked in half the initiation fee (at that time, $7,500) which seemed like a good deal. It wasn’t. What I did not calculate was the equation that includes how often I would play the course every year. As it turned out, I have averaged about a dozen rounds annually over the last 20 years and, not even considering the $7,500 initiation fee I paid, each round of golf has cost me $250 based on the average $250 per month dues I have paid through the years. (Note: Green fees for the semi-private Pawleys Plantation run an average $80 or so throughout the year.) Last year, I reverted to a social membership which retains pool access for my wife and green fees for me that are well below the average $250 I was paying (and even below the $80 public rate). In other words, if a membership deal seems too good to be true, it may be.

I told you my tale of woe (above) about paying $250 per round as a member of the Pawleys Plantation golf club. Now if I lived at Pawleys year-round, I would have played eight times a month, and the $250 in dues would have averaged just over $30 per round, still not an extreme bargain but better than what the other local public courses charge; and you can’t put a price on being treated specially as a member (bags stored, driving range privileges, “Good to see you, Mr. Gavrich” greetings from staff). I encourage clients to merge any initiation fee into the amount they have budgeted for a house and focus instead on monthly club dues, which can sneak up on you when added to HOA fees and the other costs of living inside the gates of a private golf community.

During my working years, I dreamed of a retirement in the quietest, most laid-back location possible. I had most of those daydreams while stuck in traffic on my way to work. My wife, who stayed home with our children after a career in the banking industry, had a different dream that involved a beach. I am glad I followed her lead because “remote” would have meant no access to minor league baseball, an inability to shop for meals on a daily basis — I am not a fan of freezing food — a lack of diversity of restaurant cuisines nearby or good golf courses a short drive away. Pawleys Island is somewhere in between remote and near-urban, with five supermarkets within five miles of our front gate, and a “shrimp dock” with freshly caught seafood just 15 minutes away. On the thankfully rare occasion we have needed emergency room medical treatment, two local hospitals are within 15 minutes and have provided terrific care. My advice when you look for a vacation or permanent home in a golf community is to pay attention to the distances of the things most important to you. You can do this easily online, before you make up your mind which golf communities to target and, certainly, before you invest the time and money to visit them. If they aren’t near what you need, cross them off your list. (See sidebar with proximities to local activities from some of our favorite communities.)

Whether it is a guilty conscience about moving away from family or a strategy to lure the children to visit for more than a couple of weeks a year, many couples buy an oversized 50-week a year home. Let’s face it: You love your kids and grandkids, and they love you. But that is no guarantee they will visit you in your retirement home for more than a couple of weeks (at most) every year. (You know they have their own lives, right?) In essence, buying a house that is 1,000 square feet larger than YOU need is a waste of resources. Better to find a townhouse or single-family home in your community that you can rent for your kids a couple of weeks a year or, maybe even better, a nice local hotel with a pool and other attractions for the grandkids. The visit will be even more relaxed for everyone and you can take the money you saved on the house and use it for a grand vacation every other year — for you, the children and grandchildren. They will thank you.

Glorious Back Nine: How to Find Your Dream Golf Home is available at Amazon and Barnes & Noble in both digital and paperback versions.

Larry Gavrich

Founder & Editor

Home On The Course, LLC

The following are some of my favorite golf communities with their proximities to important services and entertainment options. Whether you want total peace and quiet in a remote location, or plenty of entertainment and other options nearby, one of these communities will fill the bill. For more info on these communities or the many others that are near and far, contact me at

Six golf courses, 4,800 acres, 8,000 residents

City of Savannah – 15 minutes

St. Joseph’s Hospital – 16 minutes

Savannah Bananas baseball – 20 minutes

Tybee Island beach – 45 minutes

Two golf courses, 4,000 acres, 8,500 residents

City of Charleston – 27 minutes

MUSC Health Medical Center – 22 minutes

Charleston River Dogs baseball – 23 minutes

Folly Beach – 33 minutes

Two golf courses (45 holes), 2,200 acres,

3,700 residents

City of Wilmington – 23 minutes

New Hanover Regional Medical Center

– 29 minutes

Wilmington Sharks baseball – 29 minutes

Wrightsville Beach – 12 minutes

18 holes by Jack Nicklaus, 3,900 acres,

800 residents

City of Greenville – 53 minutes

Cannon Memorial Hospital (Pickens)

– 22 minutes

Greenville Drive baseball – 53 minutes

Lake Keowee recreation – right there

Six golf courses, 12,000 acres, 6,000 residents

City of Athens – 1 hour; Atlanta – 97 minutes

St. Mary’s Good Samaritan Hospital – 7 minutes

Macon Bacon baseball – 79 minutes

Lake Oconee recreation – right there

27 holes of golf, 1,700 acres, 800 residents (est.)

City of Norfolk – 50 minutes

Riverside Shore Memorial Hospital – 43 minutes

Norfolk Tides baseball – 51 minutes

Chesapeake Bay beach – on site

Buy It Now

Buy It Now

at Amazon.com

or BarnesandNoble.com.

Realtors across the Southeast are starving…for listings of homes for sale. This is also causing consternation among the hundreds of thousands of Baby Boomers looking to move to the region, as well as for all those employees now working from home and looking for larger homes (with a room for an office) in lower cost-of-living locations. What to do? We explore some options, as well as announce a new design for our blog site — much more mobile friendly.

Sandridge Golf Club, Dunes Course, Vero Beach, FL

Southeast golf communities remain short on supplies of homes for sale. Some realtors are on forced vacations, with little to sell; current homeowners who might otherwise list their homes for sale wonder where they are going to move. Virtually every market in the country has the same inventory shortage problem.

Options are few for those anxious to move to a golf community from a primary home they have lived in for years. Here are the major options:

With few exceptions, inventories of homes for sale are pretty tight nationwide, which means your own primary home has increased in price as well. Chances are you will downsize in retirement — kids gone, no need for all that space anymore — and you will pay less for your golf home than what your current home fetches. And your cost of living will drop, in some cases substantially, as the property taxes you pay on your golf community home in the Southeast will be half or even less than half of what you are paying now. (Example: Property taxes on a $400,000 home in Schaumburg, IL are $8,400 annually; in Leland, NC, they are $2,520. Source SmartAsset.com).

If you wait until the real estate market normalizes, you run the risk of your local market becoming “normal” before the golf community market in the Southeast returns to normal. Your home’s value may level off while your target golf home will continue to rise in price as Baby Boomers step up their searches and stay-at-home employees in the North decide they can have larger homes (extra room for an office) at lower costs in the South. That will push up demand at a time supplies are still slim. And we know what that means.

Some of the couples I work with start off thinking they need more house in retirement, or a larger vacation home, than is practical. Most of this is driven by family concerns; that is, we want our children and grandchildren to visit us as often as possible and, therefore, we need to make our house comfortable for their stays. But is it wise to invest for the exceptions rather than the rule?

Twenty years ago, my wife and I bought a condo beside the 15th tee of a Jack Nicklaus golf course in Pawleys Island, SC, located just six minutes from the Atlantic Ocean. In the last 10 years, our two children have been able to join us at the condo an average one week each year. In 2000, if we had built a house of three or four bedrooms anticipating frequent visits from the kids, it would have cost us twice as much as the condo, and we would have had all that extra unused space.

You may be thinking you need a home for your kids’ visits. You don’t. Find a community with rental properties nearby or a good family-friendly hotel. (I write this from one such hotel in Vero Beach, FL, where my wife Connie and I are quite comfortable being just 10 minutes from our son, his wife and their new baby daughter. If the situation were reversed, I know our kids would be equally comfortable and perhaps grateful that their parents are not underfoot 24x7.)

Of course, what goes up must come down, and that is true of the current housing market. But that simple law of gravity could work against you if your timing is not exquisite. Economists are predicting an upcoming spell of inflation at which time most items, including real estate, will rise in price. We don’t know whether this will drive a disproportionate number of Baby Boomers to rush South to secure their retirement homes before things get ugly, but if they get there before you do, you could find yourself priced out of the market as home prices in your target areas inflate faster than the value of your current home. Few real estate experts suggest anyone try to “time” the market, so watching and waiting may be the riskiest move of all.

Land is still relatively cheap. But, the price of lumber and construction labor costs have increased dramatically in the last two years, and a home in the Pawleys Island area, for example, that two years ago would have cost $150 per square foot to build is now estimated by local officials slightly above $200. On a 2,500 square foot home, that amounts to an extra $125,000, a premium upcharge even for a “dream” home.

But whereas you have little negotiation room on a single-family home — many are selling above their list prices — owners of lots are more flexible. Strike a good bargain and the construction costs may be a little easier to take.

Some years ago, as my wife and I were planning our retirement, I conjured a one-home solution to what we would do during the winter months. We would find a home in New England and figure out what to do in the winter months. Whereas many folks high-tail it to a vacation home in Florida from December through March (or longer) — they either purchase one or simply rent the same place every winter — I thought it would be cool if we traveled the world, perhaps staying in the Caribbean for a couple of months one year, renting a pied a terre in Paris, Athens, Amsterdam or some other interesting city another year. (The costs, I reasoned would be even less than owning a second home.) Mrs. G. was a bit cool to that idea, way ahead of me in understanding grandkids would arrive during the early years of our retirement, and the lure to visit them would be strong. (How right she was? We welcomed granddaughter Alice in early June in Vero Beach, FL, and our next grandchild is on the way in August in northern Vermont. Traveling between will take some finesse.)

Those of us who opt to stay in our current primary homes and have a substantial amount of equity might consider unlocking some appreciated value and using the proceeds to fund a vacation home. Or, if your retirement income supports it, stay where you are and just travel to someplace warm or interesting a month or two each winter.

In summary, the current tight market requires a strategy that requires some sort of action. Hesitate, as the saying goes, and all may be lost.

Larry Gavrich

Founder & Editor

Home On The Course, LLC

After 15 years and almost 2,000 articles posted, it was long overdue to “change the furniture” at our blog site, Golf Community Reviews. I had two compelling reasons — design and functionality. The site has always been easy to navigate for those who use a laptop or desktop computer. But that is an ever-shrinking proportion of our readers as many of us rely on mobile devices away from home — and some, like me, on the recliner inside our homes. On iPads and especially phones, the layout of the prior site has made navigation a headache for anyone who wanted to engage with much more than the most recently posted article.

Our new design features a more user-friendly design for both mobile phones and tablets, while retaining ease of navigation for laptops and desktops. The most recent feature story will still appear front and center on all devices; on phones and tablets, scrolling below the lead feature will bring you to the other most recent stories for easy reading. On laptop and desktop, those recent stories will appear, in chronological order, down the left side of the screen. If you are looking for a specific topic in the nearly 2,000 articles I have published in the last 15 years, an easy-to-find search tool will list states, specific golf communities, golf course architects or whatever you are looking for.

We provide other categories of information from convenient “tabs” across the top of the layout on the larger screens; on mobile devices, they are embedded in what is colloquially known as the “hamburger,” three stacked horizontal lines at top left of all pages. The burger delivers a convenient drop-down list of the “Home” page, “Contact Us,” “Subscribe” (to our newsletter), “Find Your Home Now”, “Archives” (web site and newsletters), “Links” to web sites we recommend, “About Us” and “Books,” with information on the two books I have published (one co-authored).

The new design is less complicated than the prior one and, therefore, not only easier to navigate but also more responsive. On most devices, you should see an increase in the speed of transitions from one page to the next. And as a little extra-added attraction, you can now toggle between regular mode and a “night mode” that features a black background against which white typescript is even more readable in certain lighting.

If you have any comments or suggestions about the new look, please contact me here. And thanks for reading GolfCommunityReviews.com and Home On The Course.

If you are currently looking for a golf community home, you don’t need me to tell you the pickings are slim. Recently, my wife and I drove through the sprawling community of Pointe West in Vero Beach, FL, and were impressed with its many tree-lined streets with well-tended compact homes, reminiscent of Daniel Island in Charleston, SC, and many other nicely planned communities. We aren’t looking for a home in Vero Beach but wherever I travel, I can’t help myself; I need to understand the local golf community scene.

When we returned to our hotel room, I surfed the Internet for listings of homes for sale in Pointe West, whose homes surround a rolling John Sanford layout. I follow the golf real estate markets in the Southeast pretty carefully, and I know that inventories are extremely tight, but I was stunned at just how tight. Pointe West, home to a couple thousand homes, showed just eight re-sales listed, seven of them “pending” or “contingent” on financing. Median prices for those were in the $500,000 category.

R. Horton, a nationwide builder of inexpensive homes, bought a large piece of property across a canal on the eastern side of the community and has been rapidly producing new homes as fast as they can. At attractive price points that begin in the mid $200s for homes of less than 2,000 square feet, Horton appears to be looking to sell out quickly. The price seems especially attractive for those intending to live in Florida for just the winter months. For others, “golf front estate homes” with as much as 2,900 square feet are available beginning in the mid $400s.

If you are a senior golfer, I have a book for you. It is called Playing Through Your Golden Years: A Senior’s Golfing Guide, and it was written by two guys who know what it is like to play the game at a certain age. I explain in this month’s issue of Home On The Course.

Camden Country Club, Camden, SC

What are the chances that two Baby Boomer golfers who have each published a book should meet on a blog site, wind up playing golf together and, a couple of years later, produce a book for senior golfers? In the Internet age, the odds actually were quite good.

Brad Chambers, who maintains the blog site ShootingYourAge.com and has written a book to help senior golfers do just that, has joined me in producing a brand-new book called Playing Through Your Golden Years: A Senior’s Golfing Guide. The book may or may not help you produce a score below your age, but for less than the cost of a sleeve of Topflites, it is worth a shot — or two.

Playing Through goes on sale today at Amazon.com in electronic (Kindle format) for a mere $3.99. (The Kindle app can be downloaded for free from www.amazon.com/kindleapps.)

Our new book covers all the challenges a senior golfer — male of female — faces in trying to play the best golf through their senior years. It is topical, occasionally detailed but written in a casual manner that makes the 90-pager about a 90-minute read (although a few passages are worth a re-read, if we do say so ourselves). If you are on the cusp of retirement, the book will prepare you; if you still have a few years to go, your parents will thank you for the gift.

Beth Bethel thinks we nailed it. The former publisher of the blog site Foregals was kind enough to read a review copy and wrote us the following:

“No heavy lifting, no sweaty gym sessions, no expensive training aids required. And, refreshingly, you understand and include women in your model. While you pitch to Boomers, your advice and guidance will work just as well for those of us in the Silent Generation who want to enjoy the game right up to our last breath, hopefully on the 18th hole — with the ball in the cup!”

Former PGA Tour player and Ryder Cup participant Ken Green was direct as well, saying Playing Through Your Golden Years provides all the options senior golfers need to play their best golf and have a helluva lot of fun doing it. (See the excerpt in the sidebar for more on the subject of proper tee boxes.)

We tried to combine some serious approaches to the game with the overarching principle that, above all, the game should be fun — or at least, enjoyable. For example, in our chapter on what tee boxes to choose for your round, we warn that testosterone is a dangerous thing on the golf course and keeps some of us from playing at the appropriate distances. Consider, for example, that PGA Tour golfers typically hit mid- to short-irons into most par 4 greens. Yet many of us mere mortals insist on playing tee boxes that cause us to take out long irons or even a fairway metal for most of our approach shots. Last year, I came to the conclusion that was just plain silly; I want to play like the pros — even though I don’t hit 300-yard drives (more like 200, if that). Therefore, I have moved up to the tee boxes that play between 5,600 and 5,800 yards on my favorite courses, giving myself a pro’s chance of a fair shot to the green. I am enjoying golf these days as much as I did in my grip it and rip it 20s.

Other chapters in the book include tips on how to manage a golf course when you don’t hit the ball as far as you once did; how to play as much golf as you want, including a formula for playing 12 months a year; how to stay in shape and what to do if you suffer a golf-threatening injury; the joys of connecting with men’s, women’s and couples’ golf groups; my obligatory words about finding a golf community that suits your lifestyle and your game, as well as the journey my co-author Brad and his wife Alice are starting in search of their own “best” golf community; travel golf for seniors; and a bit of advice of what to do when your golfing days are winding down.

Although the book is priced at $3.99, I am pleased to offer a free copy — in PDF format, which looks pretty slick — to Home On The Course subscribers who order my first book, Glorious Back Nine: How to Find Your Dream Golf Home, directly from Amazon. Just send me an email at

Larry Gavrich

Founder & Editor

Home On The Course, LLC

The following is a short selection from the chapter written by Brad Chambers titled “The Right Tee Boxes – for You”

We all remember what we “used” to be able to do and that includes standing on the tee with our trusty persimmon driver and crushing it 220 yards. And, yes, sometimes even 250 yards. With the wind. Downhill. But still.

Very few of us can do that anymore. Yet, the great majority of you reading this are playing from the same set of tees you’ve always played. Why? Seriously. Why???

A few years ago, I spoke to some experts on the subject, including Del Ratcliffe, a PGA Class A teaching professional and owner of Ratcliffe Golf Services which manages municipal courses in the Charlotte, NC area; two other PGA Class A teaching professionals in Lexington, KY; and Ken Green, former PGA Touring Pro and 1989 Ryder Cup team member.

Ken Green’s comments: “Golfers make the move up (in tee boxes) way too late, in my opinion. The male ego gets in the way. I don’t play the tips anymore, and sometimes I even go to the whites depending on the length of the course.”

He continues, “My theory is you should try and shoot whatever your best golf was when you were younger. I still want to shoot under par, so I go to the tee where I can shoot a few under par. Why would you want to beat yourself up playing tees where you can’t even come close to shooting what you used to shoot?” [Editor’s Note: Why indeed?]

If you are considering a search for a permanent or vacation home in a golf-oriented area, please contact me for a free, no-obligation consultation at

It is always hard to predict the direction of the U.S. housing market, but it seems like a good bet that the current shortages of homes for sale across the country, and especially in the Southeast, will not change soon. We do a deep dive in this issue. Also, fellow golf blogger Brad Chambers and I will publish a new book for older golfers in the next few weeks. In this issue, we offer an excerpt from “Playing Through Your Golden Years.”

Crail Balcomie Links, Crail, Scotland

Recently, the respected Case-Schiller Report had great news for urban and suburban dwellers looking to fetch a comfortable price for their primary homes. For many with a notion of a warm-weather retirement, that should be all they need to push them toward the Sunbelt. But there is another side to the equation.

Case-Schiller reported that home prices in the metro markets it researches had risen in January 11.2% year over year. That figure also represented a 10.4% gain over the previous month. The Phoenix metro area, favored by many retirees, led all metro districts with an annual increase in prices of 15.8%. San Diego, another retiree hotspot, saw prices rise 14.2%, the third highest rate of increase in the nation. (Seattle was #2.)

For those of us who live in metros north of the Mason-Dixon Line and are contemplating a move South, the Case-Schiller Report is equally good news. The following cities reported strong year over year price increases: Boston, 12.7%; Chicago, 8.9%; Cleveland, 11.7%; Detroit, 11%; Minneapolis, 10.7%; New York, 11.3%; and Washington, D.C., 10.7%.

That is certainly good news for many of us, but the flip side of the coin is that prices are rising just as fast, and in a few cases even faster, in the most favored areas of the South. Slim inventories and pent-up demand are behind the rapid price increases. I took a look at the end of March at listings in some of the highest-demand golf communities in the Pawleys Island area, south of Myrtle Beach; it confirmed a lot of anecdotal reporting I had heard. In Wachesaw Plantation in Murrells Inlet, for example, a community that used to be a great place for real estate bargains because of its location west of Highway 17 (just two miles), I saw only two homes listed for sale, one at $419,000 and the other at $1.9 million. (Note: Other homes were listed, but they all had either “contingent” or “pending” labels on them.) I could find just one lot available, priced just under $85,000.

A little south of Wachesaw, at The Reserve at Litchfield Beach, three homes were on the market priced between $569,000 and $919,800. The Reserve features a Greg Norman golf course owned by The McConnell Group; members have access to McConnell’s baker’s dozen of other courses in the Carolinas, Virginia and Tennessee. At Pawleys Plantation, where prices are historically more moderate than at the more private communities above, just eight single-family homes were on the market, one a “patio” home (on a ¼ acre lot) listed at $356,000 which just a year ago would have likely been priced below $300,000. The other seven were listed from $450,000 to $1.2 million, considerably higher than their values just before the pandemic began. I noted also just five lots available for sale, ranging from $62,000 up to the mid $400s.

At DeBordieu Colony in Georgetown, just south of Pawleys Island, only five homes were listed starting at $770,000 and rising into the millions. When I last looked in late 2019 at prices in the gated DeBordieu, which has its own beach as well as a Pete Dye designed golf course, I saw a few listings in the $400s.

The Pawleys Island area is not unique. At the sprawling Reynolds Lake Oconee in northern Georgia, just 11 single-family homes are listed for sale beginning in the low $600s, a couple of hundred thousand dollars higher than the lowest priced home 15 months ago. (A couple of homes with beautiful lake views are pending in the mid $2 million range.) Six cottage-style homes are available from $349,000; and if building your dream home is your thing, there are 80 homesites for sale at Reynolds from $13,900 to $3.2 million (for a lot on a peninsula jutting out into the lake).

For those who think the price increases in the South are an obstacle to moving, take a look at the property taxes on your current house and compare it to a home in your price range in a southern golf community. A home listed for sale in Pawleys Plantation for $500,000 is assessed property taxes of less than $6,000 per year. Compare that to a $500,000 home in my hometown of Avon, CT, just outside Hartford, which is assessed at nearly $12,000.

In some fine golf communities in the South, the contrast in property taxes is even more extreme. It isn’t easy to find homes for sale above $400,000 in Savannah Lakes Village in rural South Carolina; a recent search turned up just three listings above $400,000. One of them, at $479,000, carries a property tax assessment of just $1,800 annually. Combine that with the $120 per month in homeowner dues at Savannah Lakes (which includes access to the two excellent golf courses), and the run-up in southern real estate does not seem as much of an obstacle to moving.

Brad Chambers, publisher of the blog site ShootingYourAge.com, and I have co-authored a new book that will be out in electronic form this month (just $2.99 at Amazon.com). The book is called Playing Through Your Golden Years: A Senior Golfer’s Guide. One chapter of the 10 in the book deals with golf travel, and as I have been dreaming of the day I can return to Scotland and my favorite place on earth, the North Sea coastal town of Crail and the Crail Golfing Society, I include an excerpt below. Please contact me with any questions about the Society or my experiences in the true home of golf.

From personal experience, I can testify that you will benefit if you “customize” your golf trip to suit your and your partners’ tastes. Look for a unique approach to your trip, or at least part of it. I did that on my last trip to Scotland three years ago when I spent my first four days in Edinburgh. I checked into a hotel about a five-minute walk from the city’s main train station, Waverley. I had planned to play my first round at the famed North Berwick, about a 25-minute train ride from Edinburgh, and I did not want to rent a car and drive on the “wrong” side of city streets. On the morning of my round, I slung my clubs on my shoulder just outside the hotel and walked to the train station. (No one even glanced at me as I walked the city streets with a golf bag; after all, it’s Scotland.)

When the train arrived at North Berwick station, I walked 10 minutes, mostly downhill, to the golf course and had a magical round – even with the wind blowing at about 40 mph. The next day I repeated the process, although this time I took the train to Dunbar, about a 20-minute ride, and arranged for a taxi to take me to Dunbar Golf Club just five minutes away. I can’t begin to tell you how “indigenous” I felt taking a train to play golf in Scotland. It was definitely a highlight of my 60 years of golf.

Five years ago, I joined the Crail Golfing Society in Scotland. The Crail Balcomie Links golf club is the 7th oldest in the world and, combined with Gil Hanse’s “slightly” more modern (1998) layout next door, Craighead Links, it puts two of the most entertaining 18-hole layouts in the world together into one membership. If true coastal links golf turns you on, know that the sea is in view from every one of the 36 holes.

As an overseas member, I pay just $400 per year in fees, for which I receive 16 rounds of golf — eight on each layout — and the ability to host guests for just 15 pounds sterling each round. How I came to join Crail is one of the points of this chapter, but life events and a pandemic have interrupted my travel plans the last three years, and I have wound up subsidizing the Society without reaping any benefits (other than helping out a club I have come to adore). Those 16 “free” rounds this past year would have cost me a mere $25 per ($400 divided by 16) if I had been able to take full advantage. Non-members have access but pay more than $100 per round.

I am lucky, as a somewhat high-risk individual, to remain upright to this point, and I feel a bit boorish writing about not being able to travel when so many have suffered worse consequences from Covid. Golf courses in the U.S. have survived during the pandemic – many have actually thrived, perceived as safe havens for recreation and fresh air – but the story has been a little different in the U.K. with much harsher restrictions by the government that have affected golf course incomes and employment of staff and caddies. I can’t wait for things to return to normal there, for their sakes; the pandemic will be over at some point, and the all-clear will be given for people to start traveling again.

Better days ahead.

Larry Gavrich

Founder & Editor

Home On The Course, LLC

I keep hearing reports from real estate professionals and residents that the number of homes for sale in many top Southeast Region golf communities are at historic lows. (see feature story) Therefore, over the next few months, we will take a look here at the current inventory situation in communities near the coast, beside inland lakes and in the mountains of the region. First up are coastal communities and the numbers of properties for sale as of the end of March. Anecdotally, I can say that the low prices represent generally double-digit-percentage increases over prices at the start of the pandemic. That, as we know, is what happens when demand increases and supplies shrink.

45 holes of Nicklaus and Dye golf

Located 10 minutes from beach and downtown

Homes currently listed for sale: 27

Home sites listed: 11

Lowest price for home: $649,000

Highest price for home: $5.5 million

18 holes by Tim Cate

10 minutes to downtown Wilmington

Homes listed for sale: 30

Home sites listed: 31

Lowest price for home: $295,000

Highest price for home: $1.25 million

18 holes of Fazio golf

Less than 10 minutes to beach, shopping

Homes currently listed for sale: 2

Home sites listed: 1

Lowest price for home: $419,000

Highest price for home: $1.495 million

18 holes by Pete Dye

Atlantic Ocean beach inside the gates

Homes listed for sale: 13

Home sites listed: 39

Lowest price for home: $725,000

Highest price for home: $2.95 million

6 golf courses; 20 minutes from Savannah

Homes listed for sale: 59*

Home sites listed for sale: 25

Lowest price for home: $325,000

Highest price for home: $2.29 million

* includes some Skidaway Island

properties just outside the gates

Private Tom Fazio layout open to resort guests

2 minutes to beach, 40 minutes Jacksonville

Homes listed for sale: 4

Home sites listed: 0

Lowest price for home: $1.335 million

Highest price for home: $3.69 million

18 holes by John Sanford

Less than 20 minutes to beach

Homes listed for sale: 7

Home sites listed: 8

Lowest price for home: $298,000

Highest price for home: $835,000

Renting may be coming of age for retirees who want a simpler life on their “back nine.” More and more developers have jumped on the “build to rent” bandwagon, giving Baby Boomers a solid alternative to owning a home. Also this month, the McConnell Golf Group has added to its portfolio of outstanding private courses with its first incursion into Virginia just before 2020 ended.

Harbor Club, Greensboro, GA

You buy a home for personal or family purposes, you live under the roof for years, maybe decades, and one day you realize it is worth more than you paid for it. This, of course, is the “marketing tool” that the real estate industry, mortgage banks and others with a vested interest in selling real estate use to convince us all that home ownership is very much at the heart of the American dream.

It was for me and, I expect, you but now we are retired, the kids are gone, the house is too big for our current needs, and we have our eyes on a more felicitous climate in a lower cost of living area. And, of course, our first instinct is to buy a home that will be smaller, cheaper and less demanding of upkeep than our primary homes.

This is the situation my wife and I face. Now that the kids are raising their own families elsewhere — both expecting their first children within the next few months — we have too much space for our needs, and too many expenses for the upkeep on a one-acre property and 4,000 square foot house.

The equity in the house is about double what we paid for it almost 30 years ago. We plan to sell in the next year, but the quandary, even though we own a vacation condo in the South, is whether to buy yet another home or rent one. I have come around to thinking that renting either one or both homes will be more liberating – personally and financially — than owning two. And the attraction of renting is growing more interesting because of a recent surge in what is known as “build to rent” developments.

I have been carrying on for months in this newsletter, at my blog site and in my book, Glorious Back Nine: How to Find Your Dream Golf Home about the inventory shortage of homes for sale, especially in the Southeast. Those inventories are at historic low levels while demand has increased dramatically thanks to Covid, more people working from home and the still large numbers of Baby Boomers seeking their proper retirements in a warmer climate with a lower cost of living. New golf community developments are few and far between, and those who might otherwise develop them are still gun shy from the experience of the 2008 recession. But nature abhors a vacuum, and some national developers, fueled by venture capital backing and the exploding numbers of people fleeing cities for suburban and rural areas, are stepping into the breach by constructing new communities with a twist — single-family houses that are not for sale.

According to a 2020 article in Forbes magazine, “approximately 60,000 houses were being built for rent last year, and it’s not enough. From what [we are] tracking, it will rise to 75,000-80,000 in the next year [2021], and still won’t be enough to meet total nationwide demand.”

The new “landlords” are tapping into millennials’ desires for homes that meet their growing families’ needs and retirees’ needs for budget predictability. Consider that you have a home to sell, one that is larger than you need, more expensive to maintain than you want, and located in a place where winters are a burden. When sold, it will return a few hundred thousand dollars in equity to you. But you have to live somewhere, and you want that somewhere to be in a warm climate where you can play golf year-round.

For the sake of argument, let’s say the total proceeds from the sale of your home are double the $300,000 you paid for it 30 years ago, or a total of $600,000. You have two choices — buy or rent. If you buy, you can live pretty comfortably in a home — perhaps in a golf community, perhaps near excellent golf courses — for $400,000 to $500,000. On your $600,000 sale, that would leave you with a cushion of $100,000 to $200,000 in the bank. Of course, you will have other savings as well to fuel your retirement expenses.

Let us say that, instead, you pocket the entire $600,000 from the sale of your house, you invest it in a portfolio of mostly low-risk investments, and you rent one of those nice, brand new single-family homes being built to rent. Let us assume that one of those homes is renting for $2,500 per month — the average for these new build-to-rent homes, according to reports, is less than $2,000, but we will put you in one of the nicest homes. Your annual rent payments would come to $30,000.

I ran the numbers through Vanguard’s “Nestegg Calculator”: $30,000 annual rental cost, $600,000 in the “bank” and an investment mix of 50% stocks, 30% bonds and 20% cash. According to Vanguard, your money has a 73% chance of lasting 30 years, and a 50% chance of lasting 50 years (a problem if you live to be, say, 120 years old). Of course, this calculation applies only to the renting of the home, not your other living expenses, for which you will have savings (IRAs, pension income, other investments). You can also run your entire asset base in the Vanguard calculator to see how long all your money will last.

The nicest thing about renting is that there are few surprises, unless a pipe bursts but, even then, you are better off having a landlord to fix it than to have to negotiate with and pay a local plumber. Upkeep on the exterior of the home is the landlord’s responsibility, which frees you to play as much golf as you like without having a lawn waiting to be mowed afterwards. You can still enjoy the benefits of living in a planned community, including an active social life — although most of the new build-to-rent developments do not have golf courses. But there are plenty of good municipal and private country clubs nearby.

I can almost read your mind, at this point. “But Larry,” you are thinking, “you are asking me to throw money down an empty hole. At least I can be sure the house I purchase will appreciate in value over time.” And my response is a simple “Will it?” The opposite occurred during the period 2008 through around 2012, and it took a good five years for prices to come back to where they were before the recession. (Ask folks in Naples, FL, for example, or Las Vegas). In retirement, should the market collapse again, do you have 10 years to recoup what you lost? Is it worth the risk?

The positive feelings about home ownership can be, for the most part, misplaced. Consider that home you have owned for 30 years in the example above. How many repairs did you make over the decades, for example, and what did they cost? Did you redo the kitchen or the bathrooms during the time you owned the house? Add it all up and you may be surprised that the net from the sale of your house is a lot lower than you thought. My wife and I are fairly serious cooks, and a dozen years ago we undertook a massive and expensive redo of the kitchen in our now 35-year-old house. The skylights in our sunroom roof began to leak 20 years ago; that was another $5,000. My recollection is that a replacement of our central air conditioning system eight years ago cost something like $20,000. And we’ve added a deck off the sunroom which was another extreme cost. We are contemplating whether to embellish the master bathroom and adjoining area to make the house more attractive to buyers, but that will involve a low five-figure expense. All in all, when we sell the house, I do not expect to net anything. In fact, maybe we will lose a bit.

From an “investment” standpoint, how different from renting is that breakeven scenario? But my wife and I would not do a thing differently. The three primary homes we have purchased over our 40 years of marriage were based on their locations and suitability to a growing family’s needs. We never looked at each other and said, “This is a great investment” because, quite frankly, we didn’t know it was — and making money from our primary homes was beside the point anyway. We loved our three houses, we raised our two children in them and we entertained 30 family and friends every Thanksgiving for 25 years until the pandemic interrupted that tradition. Our inherent sense was that real estate always does well if your time horizon is on the long side. Ours was.

To compare renting and ownership on the basis of financial returns is a fallacy. They both provide shelter and whether a rental or owned-home is appropriate for you is more a fact of timing than financial benefit. As financial advisor Darrow Kirkpatrick wrote at his website, CanIRetireYet.com, when you own a home, “you are not in control of your monthly budget: A large home repair expense could materialize at any time.

“On the plus side,” he added, “a home is a relatively safe place to park your money: Houses are hard to steal, courts don’t like to seize them, and insurance is typically easy and cheap to obtain.”

In the last couple of decades of life, do we really want to be shackled to an asset that needs constant attention, burdens us with taxation and other costs, some of them an unpleasant surprise, and whose fragility in terms of potential repairs can fill us with anxiety? Not me, and certainly not now as I have started my eighth decade.

Of course, there are a few downsides to the rent-in-retirement approach, chief among them what your heirs will think. Buying a home that appreciates over a 20- or 30-year period — a likely proposition — means you should have equity that can be passed on once the property is sold (if you haven’t over-mortgaged it). You will need to balance that kind of legacy against the predictability and comforts of a retirement in which you rent rather than own. Also, another negative of renting is that your landlord can raise your rent at any time, probably annually unless you sign a longer-term lease. But you can accurately predict annual rental hikes. With a home you own, even with a mortgage, you also know what your annual payments will be — assuming no major repairs or a property tax hike or a mortgage whose payments are pegged to bank rates that change.

There is one other benefit to the rental scenario. Many retired couples are moving south from their homes in the northern tier of the country, leaving family and friends behind. I have written about the “two-home solution” as a way to play golf year-round in two locations. Renting one home makes it easier to live north (in summer) and south (in winter), avoiding a large cash outlay for a second home. You will still have two homes, either of which you can run to when the weather or an emergency compels you; but at least one of those homes has a fixed cost attached to it that makes financial planning more predictable.

In the end, renting rather than owning during your retirement years may provide you with what you have always wanted and deserve — the most relaxing retirement possible.

Larry Gavrich

Founder & Editor

Home On The Course, LLC

The ever-growing, ever-opportunistic McConnell Golf Group struck again in 2020, adding three courses to its already robust portfolio of private golf courses. Just before the end of the year, the organization announced a deal to purchase The Water’s Edge Country Club and The Westlake, both located alongside Smith Mountain Lake in the southwest corner of Virginia, the first McConnell properties in that state. Those purchases in December followed by a few months the acquisition of Porter’s Neck in Wilmington, NC, a solid Tom Fazio layout surrounded by mature trees and landscaping and one of the more popular communities in the growing Wilmington area. McConnell courses now span the Carolinas, Virginia and Tennessee.

The three new courses for the McConnell Group bring its portfolio to 14, all under its ownership umbrella except for the Grande Dunes Members Club in Myrtle Beach, which it manages for the development investment firm LStar.

If you are a serious golfer or golfing couple contemplating a rental home in retirement (see main feature); you like the idea of having easy access to fine private courses in the Southeast Region that were designed by legends like Donald Ross, Pete Dye and Tom Fazio; and you don’t mind driving a few hours to enjoy a day or a weekend of golf, a McConnell golf membership is worth considering. A member of any of the McConnell clubs retains privileges at all the others for no payment of green fees, just a cart rental. Initiation fees are based on which club you decide to join and range, roughly, from $10,000 to $30,000. (The amount, generally, is based on the proximity of your course to other McConnell courses; the more courses you can get to easily, the higher the initiation fee.)

For example, a couple living in a nice apartment, say, in the vicinity of Durham, NC, can count on play at Durham’s Treyburn Country Club (Fazio), Hale Irwin’s Wakefield Plantation 40 minutes away, and Donald Ross’ Raleigh Country Club, also McConnell Group headquarters, just over 50 minutes away. Slightly further afield in Greensboro are The Cardinal, a Pete Dye design, and Sedgefield, another Donald Ross classic. Greensboro is barely over an hour from Durham.

For those who prefer to own their home in retirement, many of the McConnell clubs are inside the gates of high-quality communities. (McConnell, a former software developer, has no business relationship with developers or owners of those communities but he has been invited by residents in the past to “save” their golf clubs, as he did at the floundering Reserve in Pawleys Island a decade ago and Porters Neck more recently.) The high-end nature of the private McConnell courses tends to reflect their surrounding neighborhoods and the price of homes. At Brook Valley Country Club in Greenville, NC, for example, the four homes for sale a week ago were listed in the $400s. At The Reserve in Pawleys Island (SC), the few homes listed for sale start in the $700s.

Last month I referred to the Harbor Club on Lake Oconee as “Grand Harbor,” another fine club located on a lake, in their case Lake Greenwood in Ninety Six, SC. Harbor Club is located in Greensboro, GA, a few miles from Reynolds Lake Oconee, the giant development owned and operated by Metropolitan Life Insurance Company. What Harbor Club lacks in comparative size it more than makes up for in personality, including ongoing construction of new homes at affordable prices, an active clubhouse scene and a sleek golf course designed by former PGA Tour player Tom Weiskopf and Jay Moorish. Harbor Club’s fairways were once the playground of baseball hall of famer Mickey Mantle, a one-time Harbor Club resident. Harbor Club is worth a visit should you find yourself in the area between Atlanta and Augusta anytime soon.

Now on Sale

Buy It Now at Amazon.com or BarnesandNoble.com.

If you are considering a search for a permanent or vacation home in a golf-oriented area, please contact me for a free, no-obligation consultation at

Golf community homes are on fire in the South. No, not forest fires but hot market fires, the kind that come along once in a generation when the gulf between supply and demand seems like an ocean. That is the topic this month, with some thoughts about strategies for retirees considering a move.

Golf Club of Avon, Avon, CT

The famous philosopher Lawrence Berra, aka Yogi, allegedly once said that, “When you come to a fork in the road, take it.” That pretty much sums up the dilemma faced by millions of Baby Boomers and others considering a move to a warm climate with a low cost of living. The sign on one fork points “This Way.” The sign on the other says “Stop Here.” Both choices, the only two available to those who have been planning to move in retirement, involve risk.

Covid-19 has had a devastating effect on the lives of millions and has pretty much thrown the world economy into a tailspin. Many businesses that depended on walk-in trade have been shuttered, and many more are on the brink. But two industries have not only survived but also, for the most part, thrived in ways they have not seen for more than a decade — the golf industry and the real estate industry.

Golf’s unique ability to provide recreation at an easily achieved social distance has made it a safe haven for golfers. And real estate sales have exploded, especially in areas at a distance from cities where the pandemic is at its most deadly and intimidating. And where golf and real estate are combined in warm and low-cost-of-living climates, homes are selling at historic levels.

A market environment in which prices in the most favored golf communities in the Sunbelt increased by double-digits in 2020 might argue for a watch and wait approach. After all, the laws of physics — and markets — say what goes up must come down. But the incontrovertible laws of real estate say also that when supply is low and demand is high, prices rise, and dramatically so when the delta between the two is wide.

And boy is that delta wide as I write this. A few examples should suffice. Last year, in Murrells Inlet, SC, home to Wachesaw Plantation and other popular golf communities south of Myrtle Beach, the supply of single-family homes for sale dropped by almost 33%, and in December, just 3.3 months’ worth of homes were on the market. A six-month supply is considered “healthy” by real estate industry experts. At the Grand Harbor community on Lake Oconee in Greensboro, GA, the 13 homes currently listed for sale are about half the number typically for sale historically. A little farther up the lake at Reynolds Lake Oconee, I was surprised to see recently just seven homes listed for sale; in 2019, there were dozens. But as if to demonstrate the point that the rush is on for golf homes, another seven single-family homes at Reynolds were listed as “under contract.”

At Cypress Landing in Chocowinity, NC, Dave Grahek, a member of the marketing committee of the property owner’s association board, reported that just 10 homes were for sale in the community at the end of December compared with a five-year annual average of 28. And as I have reported before, late last year the Keowee Key community on Lake Keowee in rural South Carolina reported that many homes were selling over list price and some bidding wars had erupted. A few days ago, I noted Keowee Key listed just four homes for sale under $750,000, about 1/10th of its typical inventory.

Demand for the relatively few homes for sale in Brunswick County, NC, as local Realtor Doug Terhune put it in his February newsletter, is “on fire.” New listings across the county in just the month of December 2020 were up a decent 13.6% over same-month numbers in 2019, but units sold exploded by 45.7% to a total of 577. Average selling price was just under $372,000 and the total sales volume in the county increased an amazing 65.7%, to over $214 million — in one month. That certainly meets the definition of “on fire.”

And lest anyone think it is just the lower and mid-price ranges generating the most sales, I received a report a few days ago from Kiawah Island Real Estate indicating the island, home to some of the highest priced real estate in the South, had its “strongest year of real estate sales in [its] history.” Total sales volume on the island increased 169% over 2019 figures and, not surprising, “island wide inventory is the lowest on record.” That record goes back to Kiawah Island’s first sales in 1976.

With prices rising rapidly in the most popular golf communities in the South, which fork in the road is a retiree or near-retiree couple supposed to take if they have been counting on a relocation to the warm South?

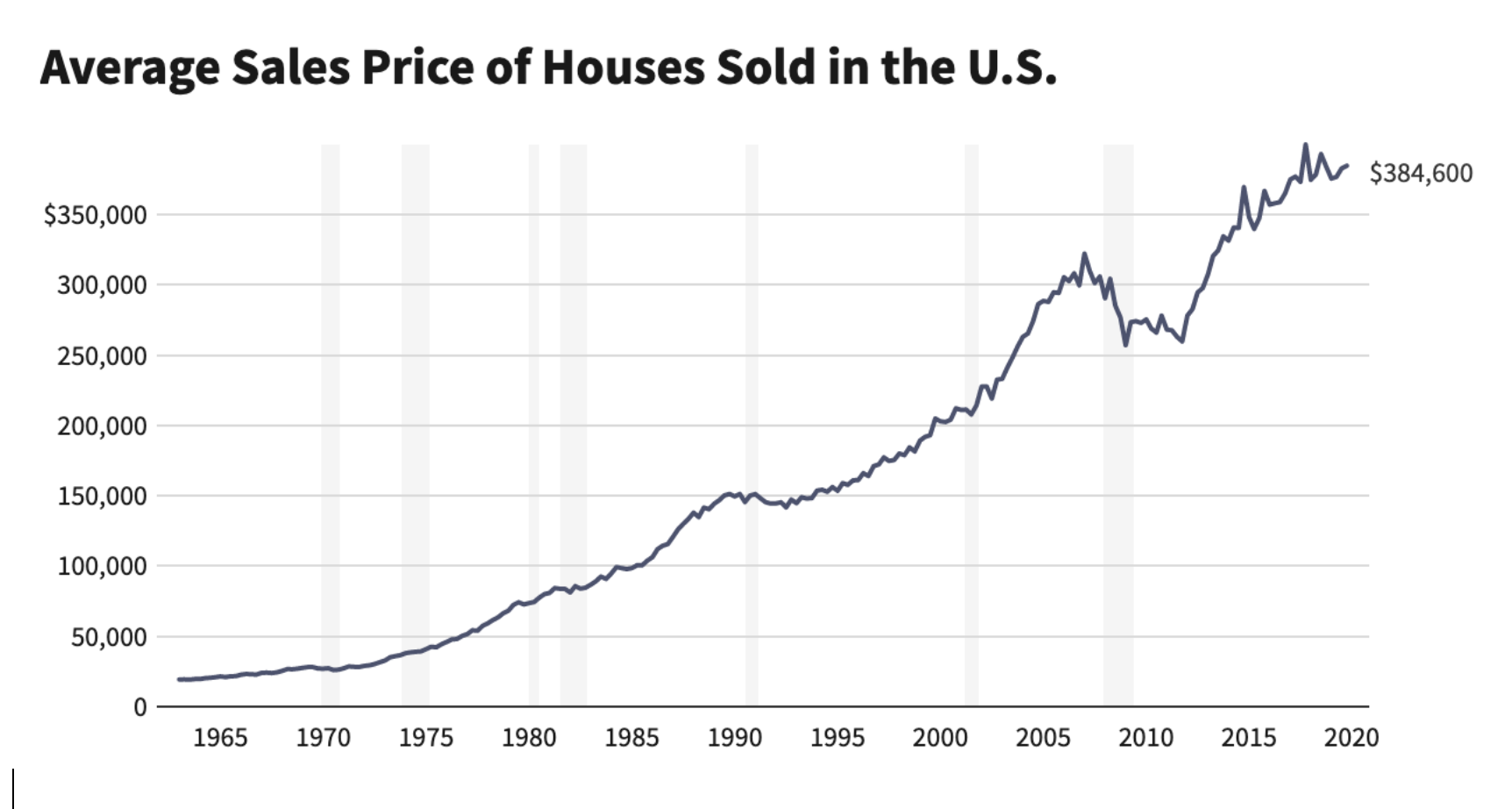

Waiting to see if the markets in the Sunbelt cool down is certainly a strategy, but it carries the greatest risk. The well-advertised notion that “past performance does not guarantee future results” may have you thinking those prices can’t keep rising at their current rates. A market correction must be in the offing, right? But the history of real estate market pricing shows that it will take pretty much an economic catastrophe to readjust prices enough to make waiting an effective strategy. The attached chart from the Investopedia website illustrates that; it shows only one significant (years long) interruption, from the beginning of 2007 to the end of 2011. Other than that, average real estate prices for homes in the U.S have risen pretty much in a straight line, from $19,300 at the beginning of 1963 to nearly $385,000 at the end of 2019.

If we encounter another major recession that readjusts home prices in golf communities, the financial lives of retirees planning to relocate will suffer in ways both related and not related to home affordability. (Think about the effects of a recession on IRAs or other investments that normally help fuel purchase of a retirement home.) And, anyway, if such a recession did not arrive for a few years, prices may have risen too much to retreat quickly enough for those who have waited. During the 2008 recession we saw prices across the South decrease by as much as 50%; they fully rebounded to pre-recession levels in about five years. Question for retirees who choose to wait: Do you want to wait five years just to get back to the price of a home you could purchase today?